Trump policy potential risks to markets

- 05 November 2024 (3 min read)

If Donald Trump wins the election and substantially raises taxes on U.S. imports, per his campaign messaging, inflation would likely go up due to the increased cost of imports that would be passed on to consumers. Although this would represent a one-off increase in prices, the rise in the inflation rate for a period would make the Fed’s job more difficult, especially if there is any indication that higher prices are destabilizing inflationary expectations, wage, and price behavior. Inflation from higher tariffs would push inflation risk premiums higher, which would lead to a steeper yield curve, higher long-term bond yields, and a shallower path of rate cuts compared to what is currently priced in At worst, the Fed would need to increase interest rates.

The secondary effect will be to slow growth as real incomes are impacted by higher inflation. Firms may also see squeezed profit margins along with like-for-like increases in tariffs on U.S. exports, which could negatively impact U.S. GDP growth. In this case, the post-tariff effect would be lower growth, which is traditionally bad for equities.

Trump’s intention to cut taxes could increase the size of the government deficit. At the same time, it may impact the private sector’s savings-investment balance if tax cuts stimulate investment and consumer spending. A higher government deficit along with a lower private sector savings surplus would mean a wider trade deficit and higher real interest rates. In turn, the U.S. would become more reliant on foreign capital inflows, which may mean a higher rate differential or a weaker dollar.

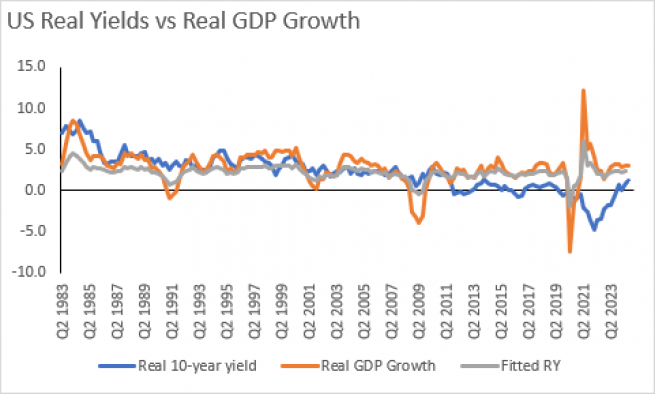

Real rates in the U.S. (Treasury 10-year yields minus inflation) were very close to the rate of real GDP growth in the 1990s and early 2000s. Since the financial crisis, real yields have generally been lower than GDP growth, largely resulting from quantitative easing. The gap between the observed real yield and a fitted model estimate, which is based on real GDP growth, turned from positive to negative around the time of the financial crisis. Today, however, real yields are just marginally below what the fitted model would suggest. An aggressive fiscal policy boosting GDP growth and raising the Federal deficit would likely push real yields higher.

The rise in Treasury yields in recent weeks has been correlated with indicators of a higher probability of a Trump victory, which have been largely anticipated by betting markets. A Republican sweep at the election could raise the probability of tax cuts and may also embolden an elected Trump to interfere with monetary policy – as has been suggested in some circles. This would be very bearish for bonds.

The chart shows real yields vs. real GDP growth and the fitted model estimate of real yields. Adjusting for the error term, the model currently suggests the neutral 10-year US Treasury yield is around 4.3% (almost exactly where it is trading a week before the election). As such, a Harris win could signal a buying opportunity in U.S. Treasuries.

Disclaimer

Risk Warning

Investment involves risk including the loss of capital.

The information has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. This analysis and conclusions are the expression of an opinion, based on available data at a specific date. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections, forecast, anticipations and hypothesis which are communicated in this material.

Disclaimer

This document is being provided for informational purposes only. The information contained herein is confidential and is intended solely for the person to which it has been delivered. It may not be reproduced or transmitted, in whole or in part, by any means, to third parties without the prior consent of the AXA Investment Managers US, Inc. (the “Adviser”). This communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

© 2024 AXA Investment Managers. All rights reserved