Investment Strategy Outlook – Shifts in the balance of risk and return

- 16 December 2024 (5 min read)

KEY POINTS

Supportive market backdrop but with new risks

U.S. President-elect Donald Trump’s radical policy agenda has created some financial market uncertainty, in terms of the outlook for investment returns. Nevertheless, we believe the central macroeconomic outlook demonstrates potential favorability for bonds and equities. Growth, stable inflation, and lower interest rates should support markets. But investment decisions should consider cashflow resilience and valuations, given policy risks and broader concerns. For now, we don’t predict a recession in 2025 – which should help deliver positive equity returns, while credit markets should provide attractive income opportunities.

U.S. policy agenda should be equity positive

Trump’s agenda creates a potentially positive growth impetus. Lower corporate taxes and deregulation should support equity markets. The extension of earlier income tax cuts and positive real income growth would underpin consumption. Despite the new administration’s expected preference for oil and gas production over subsidies for renewable energy, investment in the green transition will remain a major theme (at least outside of the U.S.) Forecasts of significant increases in electricity consumption, driven by the technology sector and China’s power demand, could promote further integration of solar and wind energy assets into power networks. Investment opportunities in sectors such as electrical components, equipment, and renewable energy production continue to be a potential option for a sustainably focused equity approach.

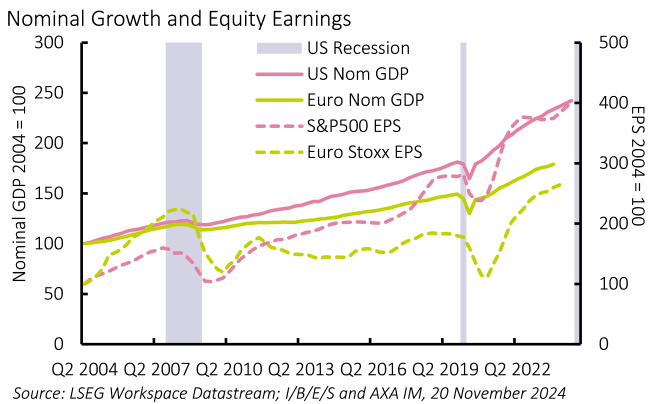

Earnings momentum could be a key driver

Equity returns have historically been positive outside of periods of U.S. recession, with an average 12-month total return of around 15%, compared to a mean return of -6% during recessions (as identified by the National Bureau for Economic Research). After solid earnings growth in 2024, the consensus forecast for 2025 is around 13% growth in earnings per share for the S&P 500. Much of this is likely to continue to be driven by the technology sector, with there being no evidence of any softening in demand for artificial intelligence (AI) related technologies. In 2024, close to half the growth in the entire market’s earnings per share came from the U.S.’s information technology and communications sectors. Policy may stimulate stronger earnings growth in areas such as financials and energy, although the impact of potential tariffs is unknown for other industries. Overall, however, U.S. equities should likely retain their leadership position. Small-cap equities could also benefit from lower taxes and interest rates with upgrades to earnings expectations already having been seen (Exhibit 1).

Mixed outlook outside U.S. borders

Elsewhere, the outlook is mixed. China appears likely to continue rolling out policies designed to stimulate domestic demand. This may be positive for Chinese equities, but any improvement will be judged against the potential negative growth impact from U.S. tariffs. A global trade war is not helpful for companies relying on exports, and performance between domestic stocks and exporters could diverge significantly. This may not be something confined to China if Trump does go ahead with tariffs targeted at many countries. Emerging market equities may find this a more difficult backdrop with a less benign U.S. interest rate outlook and a stronger dollar also being headwinds.

Europe’s growth outlook is subdued, although equities could get some support from lower interest rates and the improvement in real incomes via lower inflation. European stocks could benefit from more attractive valuations than in the U.S., and they may boast a higher dividend yield. But expected earnings growth is only about half that forecast for the U.S. Interest rate-sensitive and consumer-focused sectors should continue to perform well, with some potential upside for industrials, provided the global industrial cycle shows signs of an upturn and if the worst fears of a trade war do not materialize.

Lower interest rates may be good for bonds

Interest rate expectations define the baseline for fixed income markets. The U.S. potential policy mix has some upside inflationary risks. Moreover, inflation in some economies is settling slightly above central bank targets. Market-based expectations of terminal rates (neutral policy targets) have moved higher in recent months as a result. However, this may not be bad for bond investors. The prevailing level of yields in developed bond markets could illustrate a basis for robust income returns, which should remain above inflation.

Short duration continues to show potential

There are potential risks around longer-term interest rates coming from policy uncertainty and the profile of government debt in many countries. This has already led to a cheapening of longer-term government bonds on a relative value basis, when compared to the interest rate swap curve. For some investors, there could be potential opportunities to move out of longer-term corporate debt into government bonds, particularly for institutional investors that have an interest rate swap benchmark.

However, for short and intermediate maturities, the bond market appears to be healthy. We see yields as fairly valued, given the interest rate outlook, so much so that we believe investors are unlikely to experience similar duration shocks to those seen in 2022 and 2023. On the credit side, despite spreads being tight, the additional return and the anticipated continued healthy state of corporate balance sheets underpins the potential attractiveness of both investment grade and high yield bonds. Of course, investor sentiment towards credit will be subject to the uncertain evolution of policy and geopolitical risks, but on a risk-adjusted return basis, credit is attractive in our opinion. This is especially the case for short-duration strategies. We continue to anticipate U.S. high yield, a short-duration asset class, potentially delivering healthy returns.

Europe vs. the U.S.

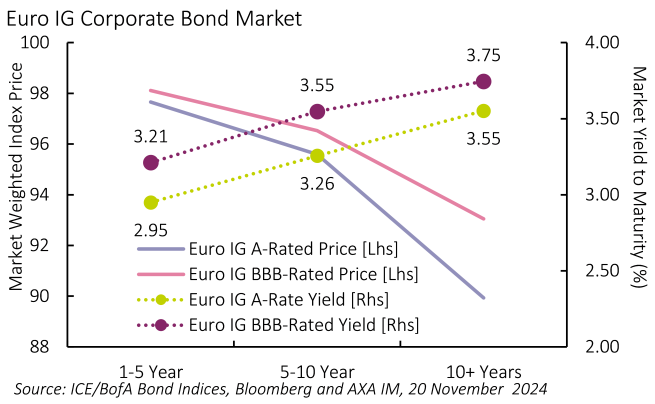

Our forecasts allow for greater monetary easing in Europe than in the U.S., reflecting softer growth. Thus, European fixed income investors may see total returns boosted by some potential decline in bond yields. Additionally, the relative picture should continue to support a strong dollar. For non-dollar investors, on a currency hedged basis, European fixed income looks potentially more attractive – especially as we continue to predict possible opportunities in the credit markets (Exhibit 2).

Risk premiums

Global economic expansion, while likely to ease in 2025, should underpin corporate earnings and support returns from equity and credit markets. However, valuations are a concern. This is particularly the case in the U.S., where equity multiples and credit spreads have reduced risk premiums. The simple U.S. equity risk premium has turned negative on some measures. Any indication that radical policy making could disrupt corporate profits could impact U.S. equity multiples, hitting total returns in the process. Given the level of yields, bonds could provide some offset to any decline in equity valuations.

Credit spreads are also tight, however. This does reflect healthy demand for credit assets which itself is a function of strong fundamentals. But again, any threat to the macroeconomic outlook could potentially push credit risk premiums higher and reduce the excess returns from corporate bonds.

Investors may consider flexibility in 2025. The benign soft landing and lower rates story helped returns in 2024. Yet, as the year closed, policy and geopolitical risks came back into focus. Tariffs, concerns about government bond supply, and trade or commodity disruptions due to geopolitical developments may be threats to discounted cashflows and therefore current valuations.

We anticipate cash returns will ease further as rate cuts continue but see income remaining the focus in bond markets and compounding returns from short-duration exposure in credit and high yield remains a potentially attractive approach in our opinion. We also see a U.S. growth focus in equities as a core with upside coming from thematic sectors like automation, the green transition, and the broader continued strong investment in technology and AI.

Source: All data from AXA IM, as of November 2024 unless otherwise indicated.

Disclaimer

Risk Warning

Investment involves risk including the loss of capital.

The information has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. This analysis and conclusions are the expression of an opinion, based on available data at a specific date. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections, forecast, anticipations and hypothesis which are communicated in this material.

Disclaimer

This document is being provided for informational purposes only. The information contained herein is confidential and is intended solely for the person to which it has been delivered. It may not be reproduced or transmitted, in whole or in part, by any means, to third parties without the prior consent of the AXA Investment Managers US, Inc. (the “Adviser”). This communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

© 2024 AXA Investment Managers. All rights reserved